Real estate is probably Sri Lanka’s oldest investment option. It has been central in growing and passing on wealth. Even marriage – one of society’s principal social contracts – was defined by real estate. Kandyan law allows for two types of marriages: diga and binna. A main difference between the two is that in a diga marriage, a woman loses her right to inherit her father’s property without the joint approval of her siblings while, in a binna marriage, a woman maintains her right to inherit property.

However, historical traditions do not always provide a basis for good decisions. So it is instructive to understand how Sri Lankan real estate has performed as an asset class. Real estate data in Sri Lanka is notoriously opaque. Currently, there is no publicly available, consistent dataset on real estate prices. The few available data points lack transparency. Any dataset can therefore only provide a directional overview of trends rather than exact figures. Nonetheless, it is a useful exercise to at least try.

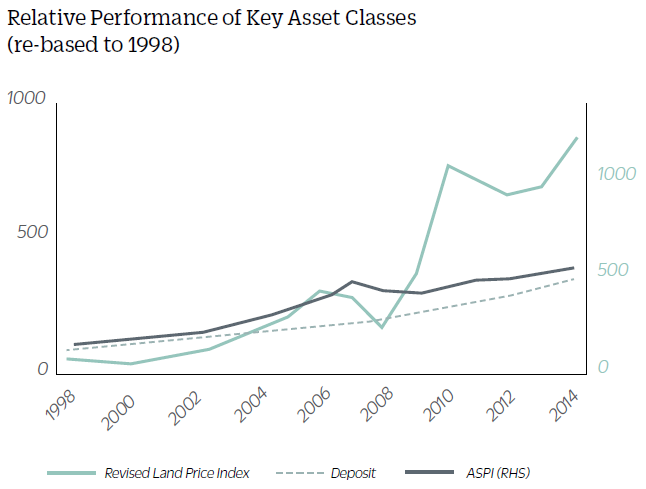

The Central Bank of Sri Lanka (CBSL) published a land price index in 2010, which unfortunately hasn’t been published since. Luckily, LankaPropertyWeb began tracking land prices in 2011. Putting these two data sets together shows that Colombo’s real estate market, similar to global markets, has delivered returns between fixed income and equity. In addition, it shows that real estate’s risk profile is somewhere in between as well. While the equity market has delivered outstanding returns, it has also been more volatile. Higher volatility creates higher risk, as money can be made or lost depending on the timing of the entry and exit. Real estate, on the other hand, has delivered steady, consistent returns. In other words, while real estate has not delivered quick gains, it has been a relatively secure, stable, wealthcreating investment.

That said, real estate also has the potential to create spectacular wealth. Of the 1,838 people on the 2015 Forbes Billionaire List, 157 owe their riches to real estate. In fact, real estate was the third-largest industrial concentration on the list, preceded by only fashion (186) and investments (161). Of the top 20 real estate billionaires, 12 hail from Asia Pacific, and they are mostly self-made, having created their wealth by riding the wave of rapid urban transformation in Hong Kong and Singapore over the past 50 years.

Currently, real estate investment in Sri Lanka, particularly beyond owning a primary residence, is an investment opportunity largely available only to individuals with some level of accumulated wealth. This is because the only viable investment option available is direct investment in real estate. Property prices in Central and Greater Colombo average around Rs4 million to Rs5 million per perch, putting direct investments in real estate beyond the reach of many. Investing in a listed property developer is another option, but there is only one focused real estate developer, Overseas Realty Ceylon PLC, and their shares are quite illiquid and therefore may not always reflect their value. In order to democratise real estate investment, the Securities Exchange Commission has been working on creating regulation for Real Estate Investment Trusts (REITs), adapting global norms to meet the high demand to develop real estate assets in Sri Lanka. This will enable all investors to participate in the sector, regardless of investment amount. Since REITs will be run by real estate professionals, they will also allow investors to outsource investment decisions to qualified asset managers.

In the interim, however, investors with the capacity to invest in real estate have to make their own decisions. This becomes particularly complex in the currently volatile political environment, which has made long-term planning challenging. Over the past nine months, Sri Lanka has moved rapidly from presumption of the continuation of economic policies that shaped the past 10 years to uncertainty regarding policy direction and stability.

In such a fluid political environment, astute investments in real estate – or really any asset – are those that are developed around themes that are likely to progress regardless of the party in power.

Currently, real estate investment in Sri Lanka, particularly beyond owning a primary residence, is an investment opportunity largely available only to individuals with some level of accumulated wealth

One such theme is the continuing urbanisation of Sri Lanka. This has been driven by the country’s transition from a rural economy to one based on services and manufacturing, a trend that began in the 1970s and accelerated over the past 20 years propelled by private sector forces, completely independent of the party in power. Over the past five to ten years, urbanisation has been shaped by infrastructure investment that has both linked and developed key cities, primarily Colombo and Galle. The Southern Expressway opened in 2011, connecting Galle to Colombo and driving up land values along the southern coast. Road and infrastructure improvements in Colombo and Galle have supported land value appreciation within the cities. The rapid rise in land values in Galle Fort is now legendary.

What will the next phase of urban development look like? Continued build-out of the nation’s highway network is likely, irrespective of the outcome of August 17. The economic transformation of the Southern coastal belt that followed the expressway has made infrastructure development a necessary component in maintaining political legitimacy. Discourse around highway development centres on how to award construction contracts, rather than whether to do so. The Colombo-Kandy highway is likely to be the next major project, as it is a key priority for both the previous and current government.

Real estate investment is ultimately executed in the details – after all, you have to buy a specific piece of land. So which plot of land do you buy? In an investment strategy designed around highway development, the forecast of the highway’s route is critical, as properties and developments closest to access points are the most likely to appreciate in value. Luckily, the current government largely endorses the trace of the previous one. The only change proposed is that the highway passes through Kadawatha as originally designed, rather than Enderamulla as was then proposed.

The other factor that will shape real estate investments based on urbanisation is the direction of urban planning. This is an area in which the approaches of the previous and current administrations differ widely. The previous government did not follow a defined plan, while the current administration has advocated a more organised approach, even collaborating with Singapore, one of the most planned of cities. Regardless of these differences, both administrations agree on the necessity of addressing Colombo’s traffic congestion. It is an economic necessity that is also likely to be quite popular.

With support from Japanese International Cooperation Agency (JICA), a Master Plan for Transport in Colombo was developed in 2014. The plan is multi-faceted and includes a monorail, as well as the modernisation of railways and the implementation of Bus Rapid Transits (BRTs) and bus priority routes. It is still too early to forecast how and when this Master Plan will be implemented in full. However, either government is likely to begin with the quick and easy wins. BRT implementation, which requires limited capital outlay but has considerable impact on commuters, is one of them. The Galle Road corridor is designated for BRTs and, given its importance, will probably be the first one to be addressed. So the already high values of property on that corridor stand to see additional benefits as it becomes the preferred location for people living in the southern suburbs of Colombo.

Real estate has delivered steady, consistent returns. In other words, while real estate has not delivered quick gains, it has been a relatively secure, stable, wealth-creating investment

Another real estate linked theme that is likely to progress, regardless of the outcome of the election, is the leisure sector, as it has been primarily driven by private players who cater to international rather than local demand. Sri Lanka has the potential to attract much more than the 2.5 million tourists currently targeted. After all, Cambodia, where almost 50% of tourists travel only to see Angkor Wat, attracted 4.5 million tourists last year, whereas Sri Lanka has a much more diverse offering. However, unlike infrastructure development, growth of the leisure industry will not follow a pre-defined plan, as it will be driven by independent actors. Choosing the right properties requires individual judgment, rather than the understanding of development plans. An analysis of Sri Lanka’s tourism trends could be informative.

One important trend is the changing composition of Sri Lanka’s tourists, who’re gradually shifting from West to East. In 2008, 45% of tourists came from the West, while under 40% arrived from the East. In 2014, this had reversed to 41% from the West and 43% from the East, primarily India and China. Growth of the number of Indian and Chinese tourists is likely to continue as the middle class of those countries becomes increasingly globally mobile. These Indian and Chinese tourists have different preferences to those from the West. First, they tend to be high spenders. Indian tourists spend 33% more on accommodation and F&B in Singapore than the average traveler. Secondly, as many travel agents in Sri Lanka note, they prefer to spend their time visiting cultural and wildlife destinations, shopping and gambling rather than on the beach. Development of properties and products that cater to this specific set of preferences is likely to see value appreciation.

In the end, real estate investment decisions are always based on the distinct dynamics that impact a specific property. These investments are inherently long-term and, while some trends are likely to continue regardless of the election outcome, the extent of their success will depend on answers to questions on Sri Lanka’s long term outlook. Will Colombo become a key urban hub of the region? Will Sri Lanka transform into the leisure destination of the East? Could Sri Lanka be a Hong Kong or Singapore in 50 years? The answers to these questions will change the way we inhabit and build out our space and, along with it, how we transform our real estate. It will also inform investment decisions and the wealth that is created along the way.

Sharini Kulasinghe is a Vice President at York Street Partners, a Sri Lanka focused boutique investment bank providing advisory services on real estate, M&A and debt and equity capital markets.