The expectation that the economy can maintain the post-war growth momentum is a foregone conclusion in Sri Lanka. People everywhere in Sri Lanka have come to expect more and better infrastructure, more government jobs and low prices. But this trend may not be sustainable.

Nishan de Mel, founder and head of Verite Research, is forecasting that rising import-led consumption will bring the rupee under pressure, and lead to a rise in interest rates and dampen the growth rate. The weakness in the island’s post-war growth has been its overreliance on construction and import-led consumption which may take a hit later in 2015 due to pressure on the currency, as interest rates rise in Sri Lanka.

Nishan de Mel shared his views about expectations for 2015 and the choices facing policymakers. Growth has been Construction – and Consumptionled “Broadly speaking, to understand our growth prospects, it’s useful to understand our means of growth. If you understand how it is that we grew a little faster after the war, then we can answer the question whether we can maintain that growth in the future.

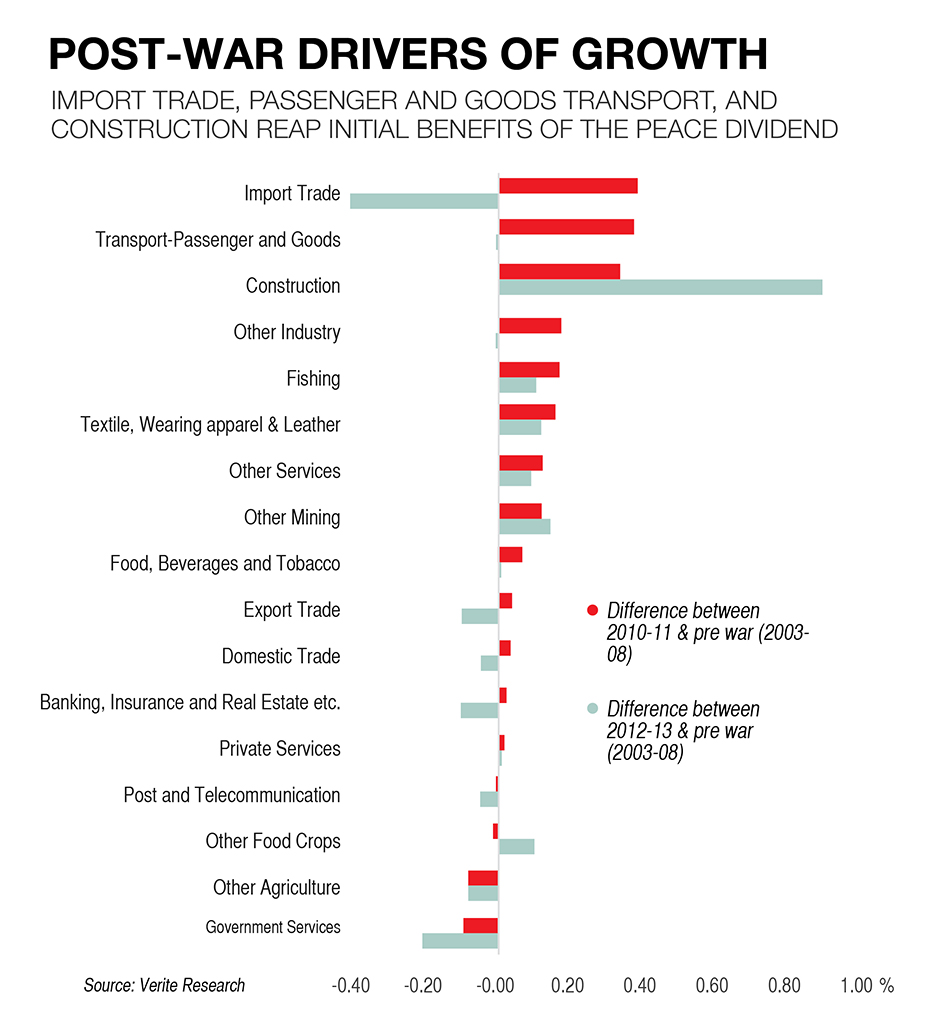

We’ve analysed government data to identify the sectors that grew faster after the war than before. There is a lot of learning that comes out of that analysis of comparing the growth of all sectors in the period before the end of the war (2003-08); to the post-war period (post 2010).

During 2010 and 2011, in the immediate aftermath of the war, what were the drivers of growth? The three largest drivers were import trade, transport in passengers & goods and construction. Post-war GDP growth was almost 2% higher. Of that, around 0.75% was added by Import trade and transport. Construction added around another 0.35% of that extra growth. Together, they added more than half of the excess post war growth. In other industries, there was a little bit of extra growth, not a great deal. What is also interesting is that the industrial sector did not grow faster. Even up to end 2013, industrial sector growth excluding construction is pretty much the same as before the war. So construction was the main part of industry that was growing. Towards the end of 2011, import trade (imported retail goods) accelerated with optimism about reaping the benefits of the peace. So people went out and purchased imported goods, and government also introduced policies that encouraged this. In the first post war budget, taxes on imported goods like vehicles were reduced. The exchange rate was also quite strong, which made imported goods cheaper.

Stability and sustainability is not secure

Optimism, conducive tax policy and an overvalued exchange rate provided a burst of import led consumption. But with this kind of burst in imports, you are going to have a problem in your trade deficit. Our trade deficit ballooned – to over 16% of GDP. This puts significant pressure on the exchange rate and the overall economic management. The government, recognizing this, started reversing policies in 2011. Tax rates on vehicles went up and there were policy reversals of import incentives. Then there was a shock currency depreciation, of three percent, announced in the budget in 2012. This still did not stem the built up pressure. By March 2013, there was another 10% plus depreciation. This again came as a shock adjustment, which generally hurts everybody. Market valuation driven changes in economic variables aren’t a bad thing, but when they don’t happen gradually and come as shocks, everyone is hurt because they can’t plan for it.

In 2012-13 import related growth crashed. So when you look at 2012-13, what is it that was driving growth? Economic growth fell to 6.4% in 2012, rose to 7% in 2013. So what were we doing better? You realize that construction became hugely important. It went from contributing 0.35% of additional GDP to 1% of extra GDP compared to the pre-war period. Everything else contributes less, except food & beverage and mining. Of course mining growth is related to construction.

Construction grew because quantity increased and also because costs were rising. When you have a lot of building projects running simultaneously, you are going to drive costs up. You can see this in per kilometre cost escalations in road projects. The per kilometre cost of the southern highway, already built at a high cost, is surpassed now by roads costing two to three times more per kilometre. It’s the same with rail, new tracks have cost four to five times more than the price at which Sri Lankan Railways expected to build them.

As a result of the breakdown of industrial growth the importance of construction has skyrocketed. It’s now over 20% of total industrial growth. Manufacturing has done less well. But by end of 2014, there were signs of manufacturing picking up. But up to 2012-13, growth was being driven by construction. That’s how post-war growth happened.

The problem in creating an import-led boom in 2015 is that the exchange rate will probably come under pressure in the short to medium term. One thing that will help release some of this pressure is the global oil price decline. But an outflow of Dollars invested in our Rupee bonds is going to cause pressure on the exchange rate. So we think this import-led growth story is not going to pan out for much more than six months. We are going to have to do some tightening. Also keeping interest rates low is going to be difficult if we are trying to manage the exchange rate. So one or the other has to start giving way at this stage if we want to prevent having another shock adjustment later. Both scenarios have repercussions.

We don’t intend to paint a picture of complete doom. I think some of the criticisms you hear about the Sri

Lankan economy going to crash are overstated. The Sri Lankan economy grew at 5-6% during the war, so there is a lot of resilience in it, and still plenty of slack that can be converted to growth. Our debt levels don’t call for the alarm bells yet, provided they keep decreasing as a percentage of GDP instead of increasing. So we are certainly not predicting that the economy will crash. At the same time the extra growth experienced post war is not sustainable either. It’s not all that bad because many economies in the world would be glad with 6% growth which Sri Lanka can yet approximate. So Sri Lanka is in a reasonably happy place. We should however be cautious against buying this overoptimistic story about growing at 7-8%. The fundamentals needed for that are not visible in the economy right now.

Pressure on trade and fiscal deficit

When government spending on construction is driving growth, it can put pressure on the fiscal deficit. To deal with this you’ve got to cut expenditure. Flawed budgeting that constantly provides over-optimistic revenue estimates means government spending comes under pressure as it maintains significant capital expenditure despite expected revenue not kicking in to keep up the spending. Encouraging imports helps the government to increase revenue, because import taxes can be around 50% of the tax revenues. This is how the fiscal side has been managed, by depending on import trade for revenue and we are seeing that cycle coming around again.

In 2014, imports started picking up again and the current budget has made many tax concessions. Worker remittances have helped keep exchange rates where they are. Remittances have grown phenomenally post war, and are now around 10% of GDP. Post war worker remittances are a large part of what has funded Sri Lanka’s consumption boom.

When you look at the fact that growth came through consuming imports, the question is how did Sri Lankans pay for it? Was it from income generated through manufacturing and exports of goods and services? Was it from borrowings? Or was it from remittances from Sri Lankans working abroad? Remember that Job growth in Sri Lanka has also been low in this period. We jokingly say that jobs were created abroad, the goods were manufactured abroad and income was earned abroad, and the only way in which Sri Lankans contributed to post war growth was by their consumption. It does not overstate the reality by very much.

If you look at the budget, the government has undertaken a vast amount of election related spending, so the growth is going to be generated from government spending and imports in the next six months. But we are going to have to consider where the growth is going to come from in the second half of 2015. Even with a lag effect, we can maybe run nine plus months. But towards the end of next year, we will have to face up to the challenge of how we are going to maintain our post-war growth story.

Weak investment trends

The other issue is that investment growth is limited. We know that to maintain 8% growth, investment should be well above the equivalent of 30% of GDP perhaps even 35% plus. Investment in Sri Lanka is struggling to reach 30%. We had a bit of an increase in investment after the war, but private sector investment has stagnated, and government investments are also static although they are higher than in pre-war years. It confirms the story that this is consumption led and not production or export led growth. Lastly, the central bank has worked hard to reduce interest rates to counter the low investment challenge. The average prime-lending rate is down to 5.5%, but credit to the private sector has not yet taken off. There are two stories behind this. One is the boost in confidence post war (to lend and borrow), saw bank non-performing loans rise. That confidence has evaporated significantly. Two is the pawning story. A lot of credit was generated here. When inflated gold prices faced a correction, it unraveled gold backed loans. It scared banks off lending against gold (which is a mainstay of the pawning sector). Low private sector confidence, higher non-performing loans at banks and the problem in the pawning sector explain why credit to the private sector has not picked up by much. Having said that, we are probably seeing the beginnings of a turnaround at this stage.

Exports lacklustre

Sri Lanka’s exports have also been falling as a percentage of GDP for quite a while. While there has been a global slowdown which is partly responsible for lacklustre exports, our share of exports in the world is also declining. If there is a global slowdown, we should still be able to maintain our share, but that’s not the case. Which means that Sri Lanka is doing worse than the average country in terms of maintaining export momentum.

The key options for Sri Lanka are around improving exports, production and services in a way that’s attractive to the world.

In increasing exports, we’ve identified two kinds of problems; of having a very few products and of having very few markets. Forty three percent of exports are apparel and 15% is tea. Everything else counts for 42%. As far as export markets are concerned, 24% is to the US, 32% to the EU and less than 50% to everyone else.

One approach to diversify export markets is to sign FTAs (Free Trade Agreements). But here is an important question: do we have few markets because we have few products? Or do we have few products because we have few markets? Which is the actual bottleneck? In our view, it’s our products that are the challenge and not markets. In the US and EU we have the right markets for the products that we have. The US and the EU are the biggest buyers of apparel, and we send our tea to the biggest buyers of tea, which includes Iran and the Middle East. So we have chosen our markets well. If we are to expand to new markets the game changer will have to be in having new products to sell to these markets. This is where Sri Lanka has been weak, post war. We haven’t shown that we can develop new products. I think government and private sector has to discover the sectors where we can win on the international stage. So far it’s the product concentration problem that is primarily constraining Sri Lanka, not the market concentration problem.

Efficiency improvements are important

Beyond exports, we have to focus on the efficiency of our economy.

The world economic forum index on competitiveness classifies countries into three segments– (1) basic factor-driven, (2) efficiency-driven and (3) innovation-driven economies. Sri Lanka is no longer a basic factor-driven economy. Our per capita GDP and cost structures put us in the range of efficiency-driven economies, so we can’t expect cheap labour and resources to be the main engine of our future growth.

That means we have to fix our supply side issues: that means fixing the technology and productivity challenges that are impairing our efficiency. Those fixes are what’s going to make our exports more competitive and get them growing. Currently, Sri Lanka’s own apparel firms are probably growing more outside of Sri Lanka than they are growing in the country. That is because the factor-driven approach won’t work anymore. Sri Lanka is still succeeding because it has entered into design and niche apparel. The private sector industry that is succeeding is doing so by leaping over efficiency problems that exist in our economy and investing in innovation.

Hard infrastructure like roads and railways improve logistics and help to Improve efficiency. But more is needed. There is the soft infrastructure like efficient public institutions, the regulatory environment, trust in institutions and transaction costs that also matter hugely for improving efficiency. If we don’t solve those structural issues in our economy, then we’ll face some difficulty in delivering sustained growth.

Budget and economy face management challenges

Many economists looking at Sri Lanka will say there are a lot of puzzles about the rates of growth that Sri Lanka is reporting. Our investment levels are too low, that’s the first point. Two, exports are low and, three, job creation is low. Growth numbers don’t make sense when you look at these fundamentals.

The budget deficit has been coming down, and that’s a good thing. Governments historically however have set targets that they don’t meet. In 2006, we had a plan to bring the deficit to 5.8% by 2009. In 2010 we revised it to 5.2% by 2012. We kept revising it. The good news is that the deficit is just under 6% in 2013. It’s been a long time coming, but we have managed to move it in the right direction. Higher economic growth is one way to reduce the deficit. It’s also then possible to increase government revenue because growth generates more economic activity. We’ve had some economic growth, but our government revenue as a share of GDP has been falling rather fast. If you compare the predicted government revenue to

the outturn it’s rather different. In 2006, 2010 and 2012, the government predicted an upward path of revenue to GDP, but it kept going down.

When you are trying to meet a deficit target as a percentage of GDP, in the context of falling revenue, you have to cut expenditure faster than the declining revenue. That’s the only way to reduce your deficit and that hurts. If expenditure is low because they’ve stamped out corruption, reduced the number of government jobs, stemmed losses at state institutions then that can be credited to efficiency improvements, but this is not the case. Instead expenditure on many essential sectors has been cut. Government spending on education and health as a percentage of GDP is at an all-time low.

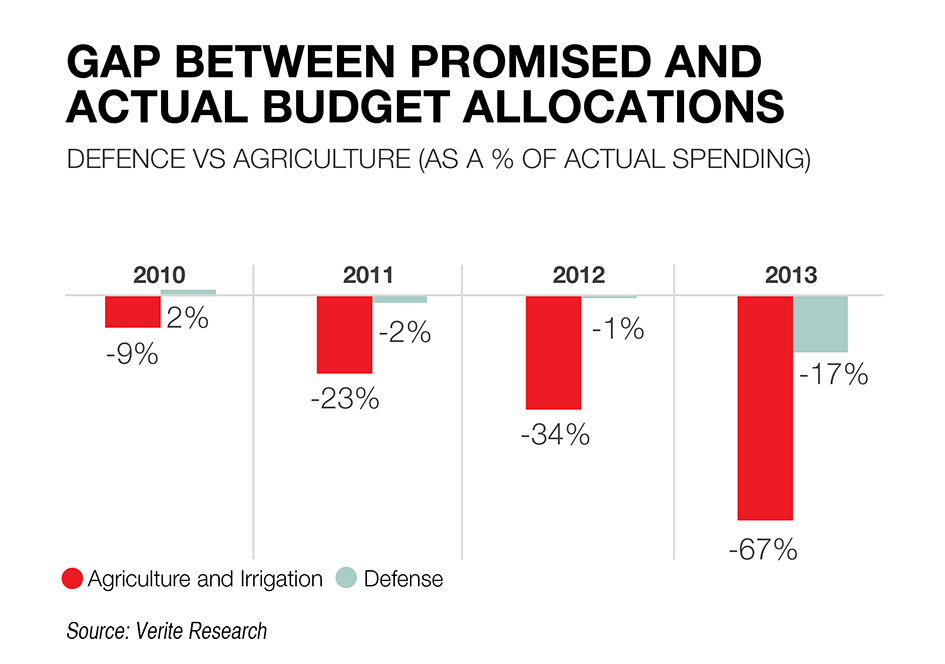

There isn’t much evidence that the expenditure cut has come from a crackdown on waste and corruption. But there is some evidence that it has come at the expense of things that deserved significant government investment and spending. For instance, if you look at what happened with agriculture and irrigation spending in 2010, it got 9% less than the budget allocation, in 2011 it got 23% less, in 2012 it was 34% less than the allocation and in 2013 it received 67% below the allocation. The only sector that held its allocation in the budget was defence. In 2010 it actually got 2% more, 2011 was 2% less, 2012 was 1% less and it was only in 2013 that it recorded a significant cut of 17%.

So to meet deficit targets some areas of the economy had to bleed, and the agriculture segment has bled more than others. But every sector has bled to some degree and this has consequences on the long-term ability to grow. If construction spending is driving growth but is costing more, and if spending in other sectors which can contribute to longer-term growth is being significantly reduced, that does create concerns about long-term economic consequences.

Additionally, the deficit target is not sustainable anymore, given the spending priorities of the current budget. There is no way to maintain that. No way to sustain the current set of election goodies and also to maintain the deficit target. The revisions they put on the budget changes what was said in the budget speech. The deficit will have to go up by at least 4% to make the spending viable. That in turn will put pressure on our credit ratings. In a sense, considering all the pressures on the fiscal side, pressure on trade deficit, and pressure on the exchange rate, there is no room to reduce interest rates either. In 2015 there will be a simultaneous build of pressures on all these fronts.

Hub strategy for growth

I understand that there is discussion of Sri Lanka becoming a hub for all sorts of things. We must understand many of these are as of yet at the level of dreams than concrete actionable plans.We see real potential in the logistics sector. This is mainly because Sri Lanka’s location makes it an attractive place for transshipment. We need to put in place the soft infrastructure in terms of regulations and processes to support the growth of this sector. As we fix these problems we could move towards some of the conditions of being a logistics hub.

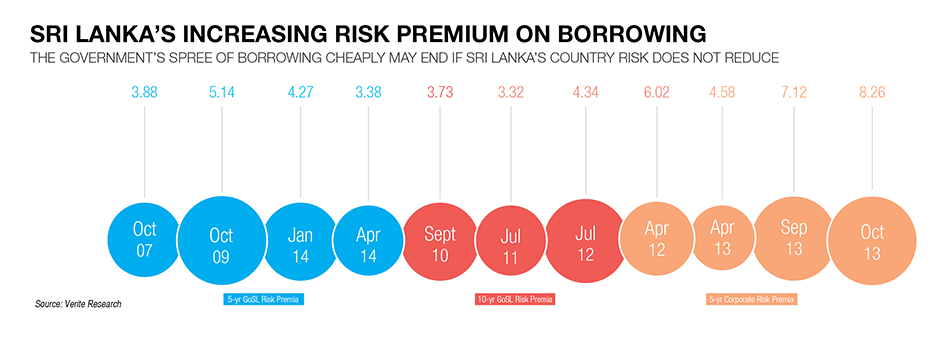

But the idea of being an education hub, for instance, is still a pipe dream. There is no sign of Sri Lanka proceeding in that path. Public investments in this area are too low. Reputation in education gets built around having very strong national universities and education institutes. Singapore and India have beaten us to it and Sri Lanka is not yet on a path that shows hope of catching up. In terms of an IT hub, it’s challenged because we just don’t have the labour force numbers to make us a mass IT services location. So we have to move into niche and high-end IT. Even our own IT companies migrate overseas, because Sri Lanka does not have the numbers. The multiple hub strategy sounds nice, it’s been on the books since the mid-90s. But it is only the logistics sector that is likely to show significant progress in that direction in the medium term.Sri Lanka has been boasting about the low interest rates at which it’s able to issue international bonds. You have to ask if we got lower interest rates because Sri Lanka is viewed as a less risky and reliable borrower, or because global interest rates are falling. The way to answer that is to look at the risk-free interest rate at the time the bonds were issued, and compare that against the bond price to figure the country risk. You can see that for 5-year bonds, in 2007, we have a country risk of 3.8%. As the war progressed, it went up, and post war it was at 3.3%, but still in the same ballpark as during the war years. On the 10-year bond, we started in 2010 at 3.73%, a good rate, and it came down to 3.32% in 2011, but went up to 4.34% in 2012. So you can see the sentiment changing a bit in the 10-year bonds. Government-controlled institutions are borrowing at high rates on the risk premium alone. Global rates are unlikely to fall from where they are now, it would seem that the only way is up. The US dollar is unlikely to fall further against other currencies over the medium term either. The spree of borrowing cheaply is going to end, unless Sri Lanka’s country risk reduces. It was probably a good move to borrow while rates were low. When rates are low, that’s the time to lock in. It’s disappointing that our risk premiums are so high, that we are unable to make the best of that opportunity. In 2012, risk free rates were at 1.27%, so paying a risk premium of 7% to borrow through government controlled entities really negates the benefit of the low rate. The inevitable increase in rates means that when we try to roll over debt, it’s not going to look less feasible than before. When looking one to two years ahead we need to do something new to maintain growth and bring stability.”