Corporate crime grows as awareness of fraud risk remains weak

White-collar crime is a growing concern in the corporate sector with a number of firms reported to have lost money when they fell victim to fraud in the last financial year. The magnitude of financial losses from fraud have also shown an alarming increase, making it all the more urgent for directors and managers to […]

White-collar crime is a growing concern in the corporate sector with a number of firms reported to have lost money when they fell victim to fraud in the last financial year. The magnitude of financial losses from fraud have also shown an alarming increase, making it all the more urgent for directors and managers to be more vigilant and ready to combat the problem.

The most high-profile fraud case to become public in recent years was that at Hayleys MGT Knitting Mills, where two top executives were arrested after a police investigation. The company, which supplies fabric to apparel manufacturers here and abroad, suffered losses and went through a restructuring.

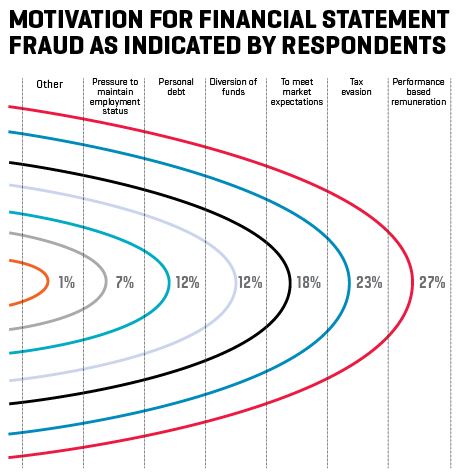

A recent survey by KPMG in Sri Lanka found that the highest loss arising from fraud was around Rs3 billion from the industrial sector and the smallest loss, of Rs2.5 million, came from the agriculture sector. “Fraud has severe consequences to the economy, the corporate sector and individuals,” says Jagath Perera, a forensic accountant who is Head of Risk Consulting of KPMG Sri Lanka. “It’s a silent crime – because there may not be gunfire, smoke or blood – but it costs you money and is invisible.” He revealed the outcome of the first fraud survey done by KMPG in Sri Lanka among directors and senior management in the corporate sector at a forum organised by the Chartered Management Institute, UK’s Sri Lanka Branch together with KPMG.

The 2012 KPMG Sri Lanka fraud survey revealed somewhat inconsistent perceptions on fraud with 83% of respondents saying they felt fraud had increased at the national level in the last two years but only 62% saying fraud in their own industry had increased in the same period. Financial positions were more vulnerable to fraud and in 60% of cases fraud had been committed by long-term employees – those with over five years of service, Perera said.

The 2012 KPMG Sri Lanka fraud survey revealed somewhat inconsistent perceptions on fraud with 83% of respondents saying they felt fraud had increased at the national level in the last two years but only 62% saying fraud in their own industry had increased in the same period. Financial positions were more vulnerable to fraud and in 60% of cases fraud had been committed by long-term employees – those with over five years of service, Perera said.

The survey found 83% of corporate fraud was done by internal parties and that 39% of people surveyed were not aware of early warning signals. The manner in which fraud was discovered also varied, with 27% by top management, 36% revealed through audits and 15% of fraud detected by accident – the last figure considered too high compared with global averages indicating lack of awareness and policies and processes to fight fraud. In fact, just over half of the respondents said they do not have a fraud risk management plan in their organisation but 70% of them had encountered fraud in their own organisations.

With economic growth picking up and the number of projects increasing, opportunities for fraud are on the increase, especially bribery such as kickbacks – payments made by vendors to employees of an organisation, and bid rigging – offers of cash or kind to get more information in competitive tenders.

“In Sri Lanka I’ve learnt a new term – the term they use is ‘we will reciprocate you’ – when you provide these additional benefits, the party will reciprocate you,” Perera said, referring to incentives offered by fraudsters to company employees to help in committing fraud. He described a ‘fraud triangle’ of opportunity, pressure and rationalisation that leads people to commit fraud.

Fraudsters first identify an opportunity and believe there’s nothing to stop them. They might also be under pressure, say to falsify figures, owing to performance targets. Finally, there’s rationalisation where fraudsters try to justify the fraud on the grounds that they’ve worked hard and earned a lot of money for the company and therefore they are justified in taking money on the sly.