Price competition remains fierce in the motor insurance segment, but the bigger companies are now clearly chasing quality business rather than fighting to expand their market share. The focus on the bottom line is good for business as well as credit ratings, says Jeffrey Liew, Senior Director Insurance of Fitch Ratings. He sees good prospects for growth in insurance given rising affluence among consumers and an aging population. With insurance penetration still very low in Sri Lanka compared with other emerging markets, the pie can only grow bigger. Prospects are attractive enough to lure foreign players as seen by the entry of AIA Group, a big pan-Asian insurer.

The shock and suffering caused by natural catastrophes, especially the Indian Ocean tsunami, is creating greater awareness of the benefits of insurance and its importance. And insurers are diversifying their product range, offering new policies to cover growing requirements like health and medical insurance and retirement planning. But, Liew warns, premiums need to be high enough to cover the cost of medical treatment as losses remain high on health insurance now. Companies need better risk management measures and re-insurance protection. Liew was interviewed during a visit to Colombo in early March for a rating review of one of the agency’s insurance clients. Excerpts:-

Insurance penetration in Sri Lanka has always been low compared with other Asian countries. What are the restraining factors?

In Sri Lanka, just like in any developing market, it will take some time for people to understand what life insurance is and its importance. Sometimes life insurance is a luxury product – you need to have excess disposable income to start buying life insurance. So when peoples’ earnings have not reached optimum levels it is difficult for them to spend extra money to buy insurance. When developing markets grow you will see insurance penetration rates gradually picking up. Also, it depends on the importance people see of insurance itself. Because in Asia we’re seeing more and more natural catastrophes happening. For example, you might have an earthquake or floods – when that happens and your valuables are actually affected, you value insurance more. People actually have to understand what insurance actually brings to help your daily life, to enable you to bring you back to where you were before an event happening.

The market has been growing, albeit very slowly. Do you see faster growth in future given faster economic growth, rising disposable incomes and lower interest rates?

I don’t agree that insurance is growing very slowly. For instance, the insurance industry grew approximately 20% in 2011. Especially after the war more players have come in and competition is increasing. As the population grows and with an aging population – that also serves as an incentive for people to buy insurance to protect their future. We’re also seeing after the war the economy has picked up, earnings of individuals have definitely improved and that’s also a good incentive for people to buy more insurance.

So I don’t think life insurance is slow compared with some developing markets. If you look at China, they were at double-digit growth before. Now they’ve also slowed down because the base has become big. Sri Lanka still has some potential to grow – especially due to an aging population and also people actually have excess disposable income to buy life insurance for protection or saving purposes.

What are the main challenges facing insurers in expanding the market?

With new regulations coming like risk-based capital, life insurance companies will expand, but cautiously. That is very good because in our view when a new regulatory regime comes, where it actually measures asset risk compared with liabilities – what RBC (risk-based capital) actually does – that potentially limits the asset growth a company will have.Especially with a life insurance company, if it grows too much they could potentially face some capital burden and they would have to put in place significant good risk management measures to ensure the risks which they have underwritten are good and not create too many problems for their overall financial positions.

The life and non-life insurance markets have strong potential to grow. Especially the life sector, which usually comes with increasingly wealthy populations in developing countries, and people gradually becoming more aware of the importance of insurance. Also, we see new players like AIA, which is a very international player, coming into Sri Lanka. So clearly I think Sri Lanka has potential to develop itself into a very established life insurance market. Non-life sectors would grow in line with GDP growth. Given the RBCs coming in in 1-2 years time, we’re likely to see potential consolidation among the smaller players not able to meet RBC standards. The bigger players should be ok. Or maybe foreign players will take the opportunity to acquire smaller players.

Do you feel that awareness of insurance is still rather low in this country?

Insurance penetration still appears to be low because for Sri Lanka it is below one percent. Insurance penetration is defined by comparing insurance premiums with GDP. For China it is 1.8%, Indonesia 1.1%. So Sri Lanka has very strong potential to grow as people become more aware of the importance of life insurance and saving and protection.

Sri Lanka has an aging population. How do you see the potential for life insurance in this market?

For countries with aging populations like Japan, there are two kinds of life insurance products – health insurance (which is gradually picking up in Sri Lanka with products offering hospitalisation and surgical benefits) and retirement planning. These are two products that usually sell quite a lot in aging populations.

Health insurance products are gradually becoming more and more popular in these countries. But I must caution life insurers when offering health insurance products – they have to be very careful in terms of their pricing because health insurance is closely correlated with medical expenses they will incur. So if they don’t charge enough premiums they could create losses for life insurance companies. So it is very important to charge appropriate premiums to reflect the expenses of the products they offer.

Are premiums charged by Sri Lankan insurers adequate?

You have to look at the combined ratio. I’ve met with a few players here. Our feedback indicates health insurance losses tend to be quite high. That indicates there’s still room to improve – you can charge more premium to more accurately reflect losses. Also, they must start to use re-insurance protection which helps to bear the cost of any medical health claims. If life insurance companies have proper re-insurance arrangements, that sometimes help mitigate the large losses from health insurance claims.

Companies need to set up proper risk management measures when offering health insurance products which are not as straightforward as normal protection plans which just cover for death. Health insurance plans should cover for medical expenses because a person could fall ill again and again and could require multiple medical treatments which mean higher expenses for the company.

In the big companies, life insurance generally is profit-making because Sri Lanka’s interest rates are still relatively high, so many life insurance companies still manage to earn a good investment return either from the fixed income investment they have or bank deposits. Also they do careful underwriting when they select the risk they write. So some of the big players are still very good.

In non-life insurance, the motor sector pricing is very competitive. Hopefully, the market would gradually become more disciplined in writing the account risk. We’re more concerned with the motor line of business under general insurance where profit margins have been squeezed lately because of the price competition. Motor insurance is always the largest contributor to the overall general insurance sector. But one thing we always have to be careful of is that the motor premium we charge needs to reflect the risk.

How do you see the big players maintaining market share especially in motor insurance given its highly competitive nature?

Some of the big players are more profit-oriented rather than being focused on maintaining market share, which we actually like. Because, optimally, if a company is very big, writing a lot of premiums but they actually undercharge compared with the risk which is underwritten in the books – we feel that is not an appropriate thing to do. Market share is just the top line. Nowadays, when you talk with insurance companies in this part of the world, even in Sri Lanka, the big players are more profit-oriented and not so much going for market share. They are looking for quality business for which you need to charge appropriately for the risk you are underwriting. So although we see the market share of some players actually shrinking, their profit margin has been maintained or has even improved. We see this as a good thing because, overall, it’s the bottom line that counts towards the company’s financial condition, not the top line.

How will recent import duty hikes on motor vehicles affect motor insurance?

Yes, the market will be affected. Motor insurance depends on the number of vehicles on the roads. Imported cars tend to be more expensive and so for replacement, the premiums tend to be higher. Although motor is a major business it is not the only business. There are other lines of business like property and fire and personal accident business which are also improving. We know some firms want to go into personal life business which consists of personal accident and some of the critical illness life insurance products. Personal accident business outside Sri Lanka that we’ve seen is always profitable

Given the potential for some shrinkage in motor business, there could be other new lines of business which could be more profitable like personal insurance that could gradually replace motor, although it will take some time. There’s potential for mixing life and non-life into a policy offering to the client.

Companies have been relying on investment income to compensate for underwriting losses especially in the motor segment but such opportunities may not continue. How do you see them coping?

Insurance companies now are focussed on underwriting. If you are just based on top line growth and you are not really carefully looking into your underwriting profitability, you may face a situation when you don’t have investment income to support you, you may make losses. But now we see most of the big players are aware of this situation and are actually willing to forgo unprofitable business and focus more on generating underwriting profitability. In motor there’s always price competition among some of the smaller players who might undercut to get business and market share but could still generate losses. But big players are aware underwriting profitability is the key to success and are willing to forgo top line growth and focus on writing good quality business. That’s a good thing. From a rating perspective, we always view company focus on underwriting profitability as the key to success for running a general insurance company. Investment income is good to have but could be volatile and subject to market cycles.

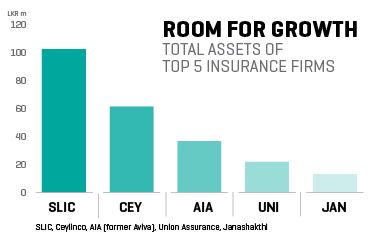

Fitch rates Sri Lanka Insurance Corporation, the biggest player. Has SLIC been able to retain its market share?

They have maintained it for certain life insurance businesses. But in some sectors there is a marginal drop. Companies sometime chose purposely to reduce market share because they want quality business. SLIC is one firm that is actually prepared to walk away from non-profitable business and maintain good bottom line. That is also what we value in this company. This company is a good company. That’s why it was rated at current levels. (Fitch rates SLIC at AA(lka)).

In previous reports Fitch has drawn attention to SLIC’s large equity exposure and their investments in non-subsidiary businesses like hotels and gas. How do you view these investments?

We do say clearly in our reports it is always something we are concerned about. Because normally outside Sri Lanka, life insurance companies cannot invest in non-core business. But they are using shareholder funds, not life funds, to invest. So that makes it much better because it is shareholder funds – and ultimately it is a shareholder decision as to what sort of investments they want. However, we do indicate that this is something we’ll keep an eye on. And that clearly has also been reflected in our rating level when we assign a rating for the company. But a company has the right to choose what they think is most appropriate for them.